Lloyds Share Price Breaks Through £1 Barrier: What’s Driving the Rally?

Historic Breakthrough for Lloyds Banking Group

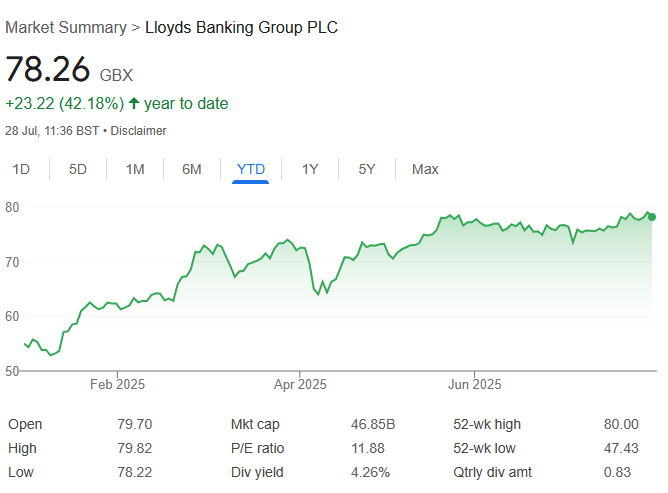

Lloyds Banking Group’s share price closed at 101.80p on 15 January 2026, representing a 0.74% increase, marking a significant milestone as the stock breaks decisively through the psychologically important £1 level. This popular and widely held stock is up 85.4% over one year and a whopping 171.2% over five years (excluding dividends), making it one of the FTSE 100’s standout performers.

The breakthrough comes after Barclays analysts lifted their 12-month target to 120p, signalling renewed confidence in Britain’s largest retail bank. The surge has brought Lloyds’ market capitalisation to over $80 billion, making it the 14th biggest company in the UK.

Why Lloyds Shares Are Climbing

Several factors are driving the impressive rally. Barclays analysts predicted “sector-busting EPS growth of 70%” by 2028, which is twice the expected industry average and 20% above City consensus. The bank has demonstrated resilience in a challenging environment, with net income rising 6% in the nine months to September, whilst its net interest margin was also up 10 basis points year on year at the end of the period, at 3.04%.

A pivotal development was the UK Supreme Court’s decision overturning a previous judgment that could have resulted in substantial compensation claims against lenders, including Lloyds, alleviating concerns about potential financial liabilities from motor finance mis-selling claims.

Income Opportunities for Investors

Lloyds remains attractive for income-focused investors. In 2026, dividends are expected to reach between 4-4.29p per share, with a yield of around 5.8%, representing growth of 17%-19%. Payouts are currently covered more than twice by earnings and backed by a rock-solid CET1 ratio of 14.3%, suggesting the dividend policy remains sustainable.

The bank is also returning capital through share buybacks, which both underpins the share price and gradually reduces the share count, improving per-share earnings and dividend capacity over time.

Risks and Challenges Ahead

Despite the positive momentum, analysts have identified several headwinds. Threats like rising credit impairments and weak loan growth are severe as the UK economy struggles. Revenues and net interest margins (NIMs) are also under threat as competition accelerates in Britain’s banking industry.

The company announced £800 million charge for motor finance commission, bringing the total amount to over £1.7 billion, though the Supreme Court ruling has capped the worst-case scenario. Additionally, analysts expect UK growth to slow in 2026, with rising unemployment and increasing personal and corporate insolvencies being two worrying omens moving into the New Year.

What Analysts Are Saying

The analyst community remains cautiously optimistic. Analysts are mostly upbeat, with an average 12-month price target of 103p — suggesting a moderate gain from current levels. However, there’s considerable debate about valuation. The analyst narrative has Lloyds Banking Group modestly overvalued at a fair value of £0.96 versus the £1.02 share price. The DCF model, however, suggests fair value of £1.68, which is a 39.2% gap above the current price.

Some analysts express concern about stretched valuations after the dramatic rally. The bank’s price-to-book (P/B) ratio is an enormous 1.5 times, far above the 10-year average of 0.9, suggesting the shares may have run ahead of fundamentals.

Outlook for 2026

The path forward for Lloyds shares will likely depend on execution across several key areas. Investors expect better 2026 momentum if costs stay controlled and credit quality holds up. The next key catalyst to watch will be earnings, which will come out on January 29, providing investors with updated guidance on net interest margins, loan growth, and capital distribution plans.

With the stock now trading above £1, Lloyds has reclaimed a level not seen since the financial crisis. Whether this momentum can continue depends on the bank’s ability to navigate margin pressure from falling interest rates, maintain asset quality in a slowing economy, and demonstrate that its strong franchise can continue delivering sustainable returns for shareholders.