The Importance of Business Rates for UK Enterprises

Introduction

Business rates, a tax on non-domestic properties, play a crucial role in funding local services in the UK. Understanding this topic is essential for business owners and stakeholders, particularly in the current economic landscape marked by both challenges and opportunities. With the recent government discussions aimed at reforming business rates, the significance of this tax is more pronounced than ever.

Current Developments

In the face of rising costs and changing retail environments, the UK government has announced a review of the current business rates system to ensure it aligns with contemporary economic realities. As of October 2023, many small and medium enterprises (SMEs) are expressing concerns about the heavy financial burden of business rates, especially following the disruptions caused by the pandemic.

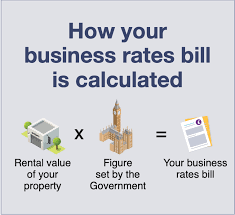

The valuation process, used to set business rates, is currently under scrutiny, with advocates calling for a more frequent assessment to reflect property market changes. Many believe that the existing framework disproportionately affects high street businesses while favouring online retailers. These sentiments have sparked discussions at local council meetings and echoed in parliamentary debates.

Impact on Businesses

The implications of business rates reform are steep. According to a recent survey conducted by the Federation of Small Businesses (FSB), 60% of small businesses indicated that high business rates make it difficult to grow. With many operators facing increased expenses amid inflation, a reassessment of how rates are calculated is more urgent. Additionally, sectors such as hospitality, retail, and leisure — which have been significantly impacted by the pandemic — may require targeted relief measures to aid recovery.

Moreover, local government budgets are critically dependent on business rates revenue to maintain essential services and community projects. If a significant overhaul occurs, it could lead to unforeseen consequences on funding allocations for local councils.

Conclusion

The ongoing dialogue regarding business rates illustrates their fundamental role in the UK economy. As the government reviews the system, businesses and local authorities must remain informed and engaged to advocate for changes that support both community services and the viability of enterprises. The future of business rates reform is uncertain, but proactive engagement from business owners will be essential in shaping a fair and sustainable tax system that reflects the needs of all stakeholders involved.