OECD Criticism of UK Tax Policy: Key Issues and Implications

Introduction: Why OECD UK tax policy criticism matters

Tax policy shapes public services, business decisions and household incomes. Criticism from the OECD — an influential international economic organisation — carries weight because it reflects comparative analysis, global standards and best practice. Attention from the OECD can influence Government choices, investor confidence and ongoing international negotiations. Understanding the nature of OECD UK tax policy criticism is therefore relevant to policymakers, firms and citizens alike.

Main body: What the OECD has highlighted

International tax and corporate behaviour

The OECD has raised concerns in recent years about how tax systems respond to cross‑border business activity. Its work on global tax reform has focused on ensuring large multinationals pay tax where value is created and on curbing profit‑shifting. While the UK has participated in OECD‑led initiatives, the organisation’s commentary has emphasised the need for continued alignment between domestic rules and international agreements to avoid loopholes and harmful tax competition.

Fairness and distributional impacts

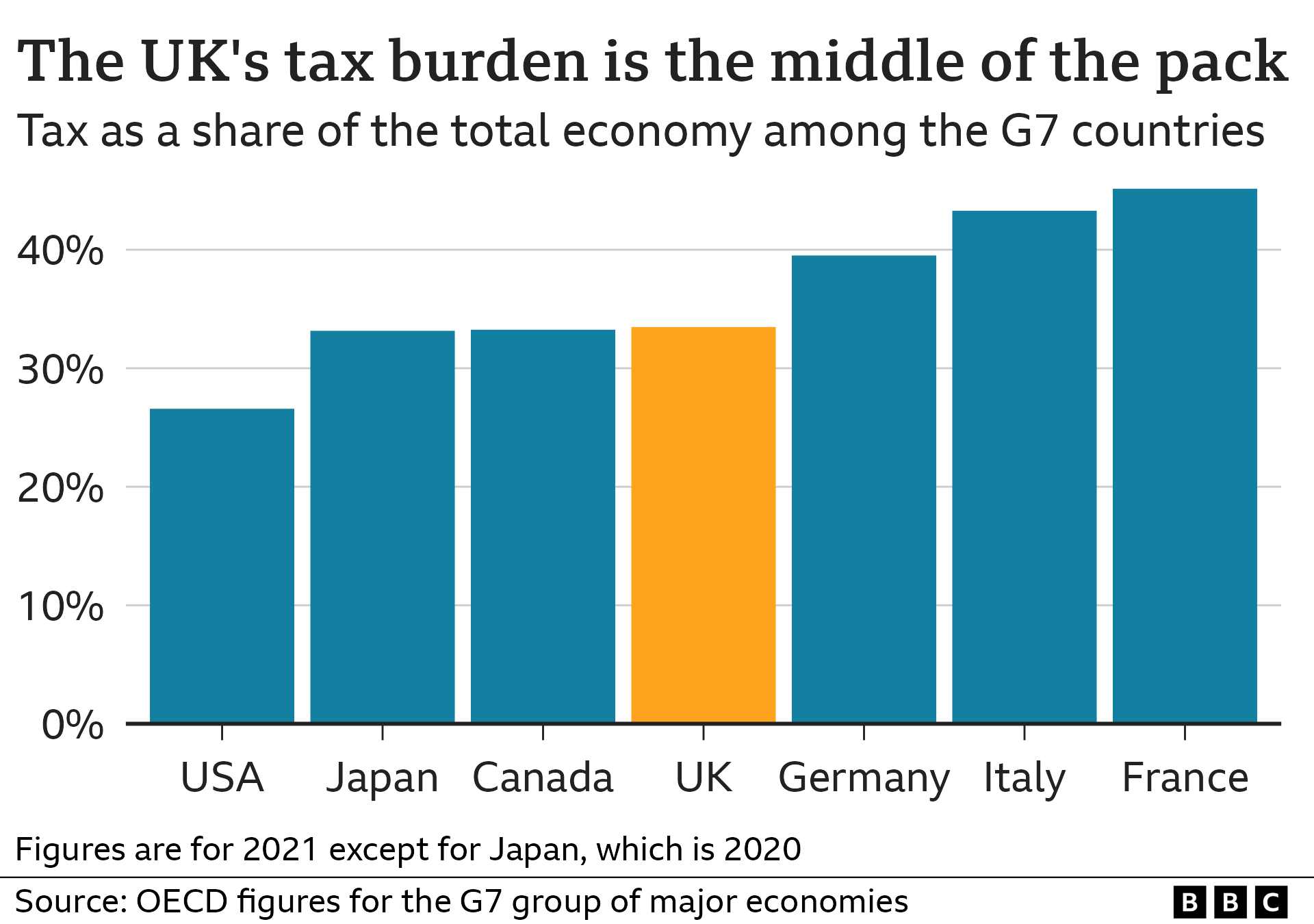

Another strand of OECD criticism relates to the distributional outcomes of tax and benefit systems. The organisation has periodically urged countries to assess who bears the burden of taxation and whether the mix of income, consumption and property taxes supports equity and efficiency. In the UK context, these observations point to debates about how tax design affects households at different income levels and how to balance incentives for growth with redistribution objectives.

Complexity, compliance and enforcement

Complex tax rules and gaps can undermine public revenue and public trust. The OECD frequently highlights the importance of simplifying tax systems, closing avoidance channels and ensuring adequate resourcing for tax authorities. For the UK, this translates into scrutiny of measures to reduce the tax gap and strengthen enforcement, alongside efforts to keep compliance burdens proportionate for businesses and individuals.

Conclusion: Implications and likely direction

OECD UK tax policy criticism signals areas where reform or closer alignment with international norms may be expected. For readers, the practical implications include potential changes affecting businesses’ tax planning, household tax liabilities and the design of environmental or wealth‑related taxes. Looking ahead, continued OECD engagement is likely to shape debate as the UK balances competitiveness, revenue needs and fairness. Policymakers will need to weigh these trade‑offs while communicating clearly with stakeholders about planned changes.