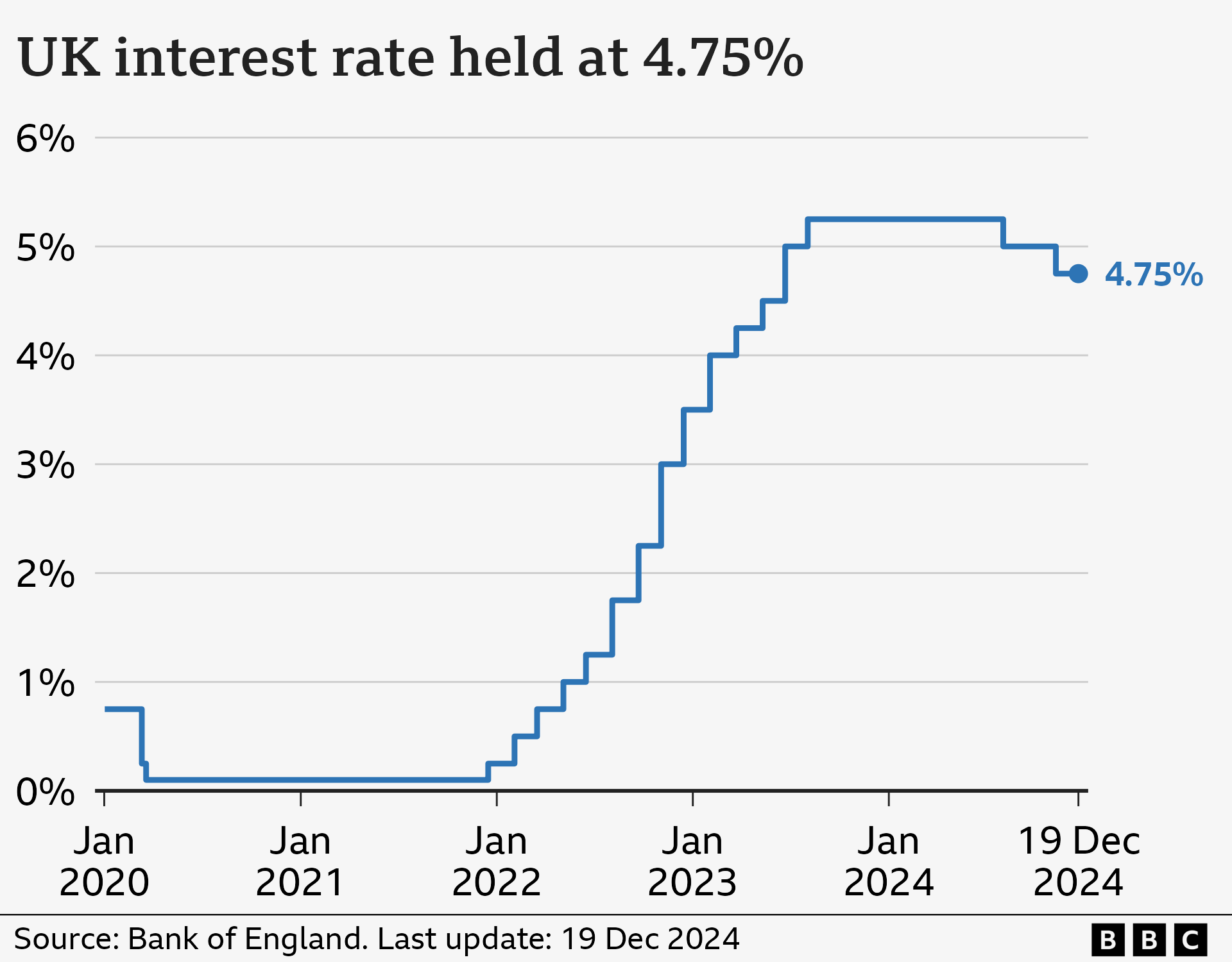

Bank of England base rate at 3.75% after December MPC

Introduction: Why the Bank of England base rate matters

The Bank of England base rate is a cornerstone of UK monetary policy and directly affects the cost of borrowing and the return on savings. The rate set by the Bank’s Monetary Policy Committee (MPC) influences mortgage and loan rates offered by banks and building societies, and so has a tangible impact on households and businesses across the country.

Main body: Latest decision, effects and context

Current rate and recent decision

Following the most recent MPC meeting on 18 December 2025, the Bank of England base rate stands at 3.75%. The base rate is the interest rate the Bank of England charges other banks and lenders when they borrow money, and the 3.75% level is the official short-term benchmark used across the financial system.

How the base rate affects mortgages and savings

When the base rate rises, it normally leads to higher rates on mortgages and loans offered by banks and building societies; conversely, a lower base rate can ease borrowing costs. In recent years the base rate has increased considerably, and mortgage rates have broadly moved in step with that trend. Savers may see their returns adjust more gradually, but the base rate remains a key determinant of savings account interest rates.

Historical note and possibilities

Commentary and data on the Bank of England base rate typically reference its movements over long periods (for example, changes from 2008 to 2024). While the base rate has been volatile in recent years, the Bank has previously noted theoretical options such as negative interest rates, although that scenario has not occurred to date.

Conclusion: Implications and outlook

The current 3.75% Bank of England base rate will continue to frame borrowing and saving decisions for UK households and businesses. For mortgage holders, especially those on variable deals, the base rate remains a primary driver of monthly payments. Savers and borrowers should watch future MPC statements for indications of changes. Any adjustment by the Bank will have prompt knock-on effects across the banking sector and the wider economy, affecting affordability, investment and financial planning.