Britain gas supply: current state and future challenges

Introduction: Why Britain gas supply matters

Britain gas supply is central to daily life, heating homes, powering industry and balancing electricity grids. With gas still a major component of the UK energy mix, concerns about security of supply, price volatility and the transition to low‑carbon alternatives make the topic highly relevant for households, businesses and policymakers.

Main developments and current situation

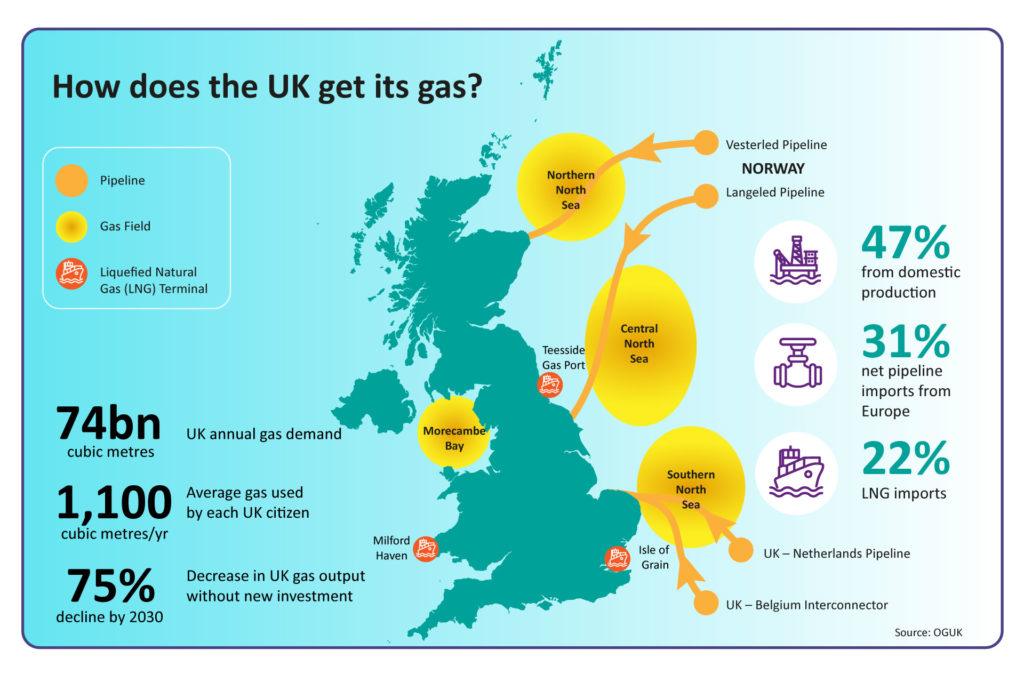

Domestic production of natural gas has fallen from its peak years, increasing the need for imports to meet demand. Britain now relies on a mix of pipeline imports and liquefied natural gas (LNG) cargoes to cover shortfalls. At the same time, seasonal demand — especially in winter — and global gas market developments influence availability and prices domestically.

Drivers and risks

Several factors shape Britain gas supply. Geopolitical events and international market tightness can push prices higher and make securing cargoes more competitive. Weather extremes raise demand for heating, putting pressure on supply during cold spells. Infrastructure constraints, including limited gas storage capacity compared with some continental neighbours, also mean the UK can be more exposed to short‑term shocks in global supply and demand.

Policy and market responses

Government and industry measures aim to improve resilience. These include maintaining diversified import routes, commercial arrangements with suppliers, and market tools to allocate gas when supply is constrained. Longer term, decarbonisation policies — such as increasing energy efficiency, electrifying heating, and developing low‑carbon gases (including hydrogen and biomethane) — are intended to reduce reliance on fossil gas.

Conclusion: What this means for readers

For consumers and businesses, Britain gas supply will continue to influence energy bills and operational costs while the energy system transitions. In the near term, diversification of imports and prudent market management are key to avoiding disruptions. Over the medium to long term, policies that cut demand and introduce low‑carbon alternatives will be central to reducing exposure to international gas market volatility and improving energy security.