BAE Share Price Rallies as Defence Sector Strengthens in 2026

Introduction: Why BAE Systems Matters to Investors

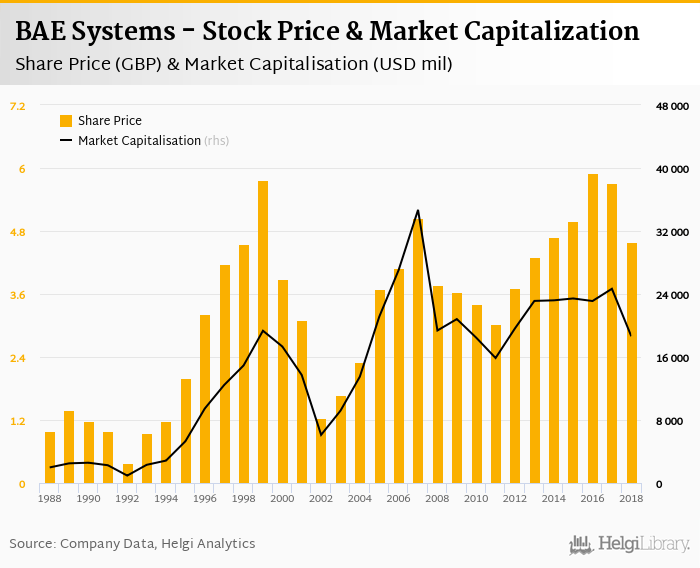

BAE Systems plc, one of the world’s largest defence contractors, has captured significant investor attention in early 2026. BAE Systems shares closed up 5.53% on Monday at 1,851 pence (£18.51), whilst BAE Systems rose as much as 6.9%, leading a broad rally in defence shares after President Donald Trump said he would request an increase in the US military budget. The company’s performance reflects growing confidence in the defence sector amid rising geopolitical tensions and increased NATO spending commitments.

Recent Share Price Performance and Analyst Ratings

The BAE share price has experienced notable volatility in recent months. BAE Systems’ share price increased 63.47% over the past twelve months, reflecting investor confidence in the company’s strategic direction and contract wins. However, the stock remains below its 52-week high of 2,071 pence, presenting what some analysts view as a buying opportunity.

Analyst sentiment has been mixed but generally positive. Kepler Cheuvreux upgraded BAE Systems from Reduce to Hold on Tuesday, whilst raising its price target to GBP18.60 from GBP15.40. Meanwhile, Morgan Stanley raised its price target on BAE Systems to GBP22.03, maintaining an Overweight rating. However, Bernstein downgraded BAE Systems from Outperform to Market Perform, citing expectations of underperformance during the European recovery.

Major Contracts Driving Growth

Recent contract wins have bolstered confidence in BAE’s revenue prospects. BAE Systems has been awarded two defence contracts totalling approximately $215 million, including a $198.4 million modification from the U.S. Department of War for Armoured Multi-Purpose Vehicles. Additionally, the company secured a $150 million contract for its active protection systems, struck in partnership with Elbit Systems, involving the integration of the “Iron Fist” defence system into CV90 infantry fighting vehicles destined for European NATO members.

2026 Outlook and Investment Considerations

Looking ahead, current analyst consensus projects revenue growth of around 7–8% for 2026. The investment case is underpinned by structural factors beyond short-term conflicts. Last June, non-US NATO members agreed to lift defence budgets to 5% of gross domestic product by 2035, up from 2% last year, equating to $423bn in additional annual spending across non-US NATO members alone.

On Investing.com’s consensus page, 18 analysts cover the stock with a consensus rating of Buy (14 Buy, 4 Hold, 2 Sell) and an average 12-month price target of 2,120.67p, suggesting significant upside potential from current levels.

Conclusion: Strategic Positioning in a Growing Market

The BAE share price reflects a company positioned at the centre of a multi-year defence spending cycle. Whilst recent volatility has created entry opportunities, the structural drivers—increased NATO commitments, major contract wins, and strong earnings forecasts—suggest sustained momentum. The next significant milestone will be the release of preliminary full-year 2025 results, scheduled for the end of February, which should provide further clarity on the company’s trajectory. For investors seeking exposure to defence sector growth, BAE Systems represents a compelling opportunity with both near-term catalysts and long-term fundamentals supporting its investment case.