UK Mortgage Rates in December 2024: What Homeowners Need to Know

Current State of UK Mortgage Rates

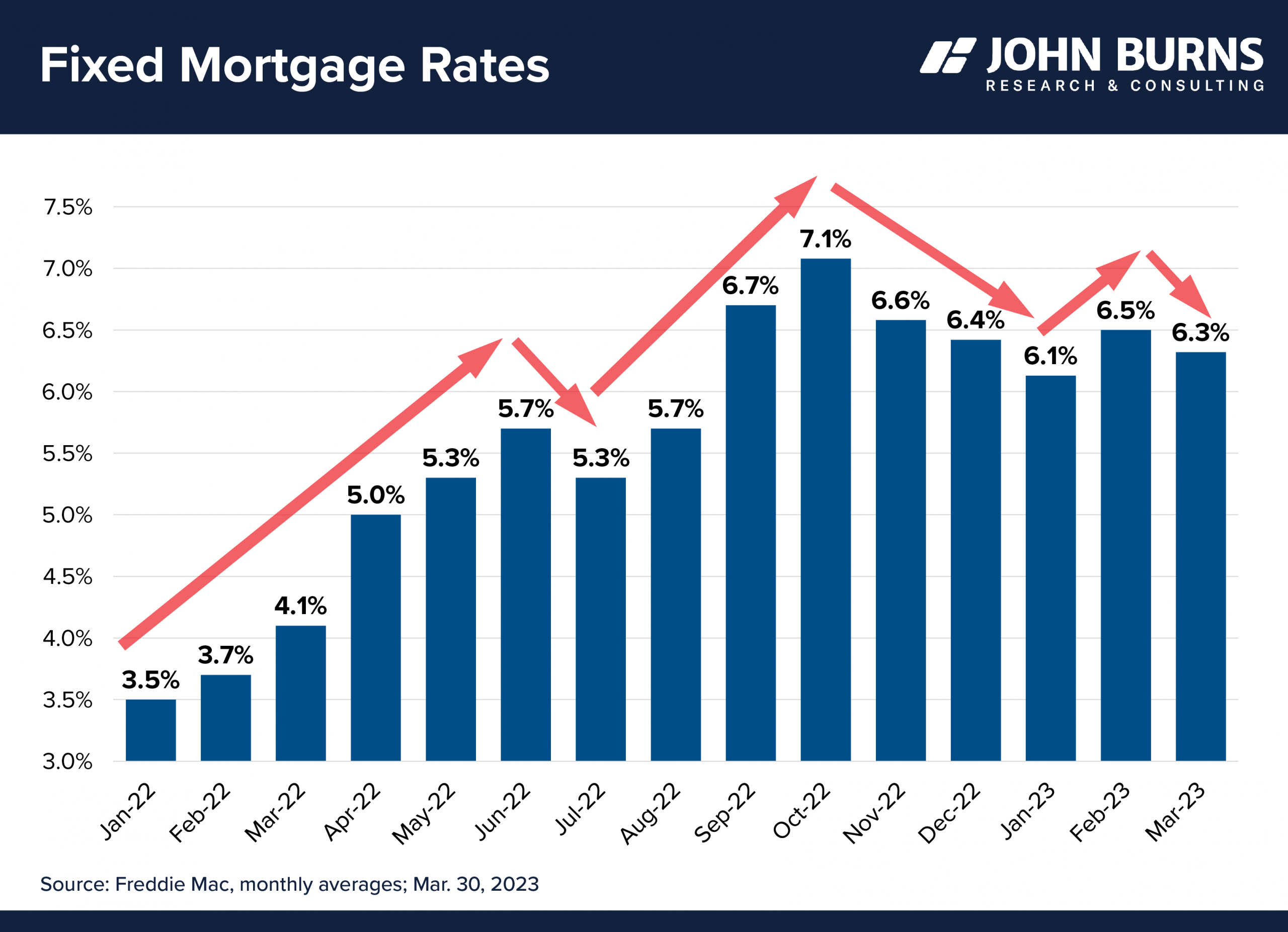

The UK mortgage market is experiencing a period of cautious optimism in December 2024. Mortgage rates edged higher before nudging back down, despite the Bank of England’s decision to hold interest rates at 4.75% on 19 December. This decision follows a November rate cut that brought the base rate down from 5%, where it had remained since August 2024.

For homebuyers and those remortgaging, the lowest average rate for a two-year fixed mortgage in 2024 was 4.6%, while the highest was 5.2%. Meanwhile, five-year fixed mortgage rates varied between 4.2% and 4.7% throughout the year. These fluctuations demonstrate the ongoing volatility in the mortgage market, influenced by swap rates and economic uncertainty.

Changing Borrower Behaviour

An interesting trend has emerged in borrower preferences. Research by Santander found that more mortgage borrowers are opting for shorter fixed deals, with 65% of customers choosing a 2 year fixed rate mortgage in the final three months of 2024, compared to 27% choosing a 5 year fixed rate mortgage. This represents a significant shift from recent years when borrowers favoured the security of longer-term fixes.

This change in behaviour suggests that homeowners are betting on further rate reductions and want the flexibility to remortgage sooner to take advantage of potentially lower rates in the near future.

Future Outlook and Predictions

Experts anticipate the Base Rate will remain at 4.75% in December, with further reductions expected in 2025, and by Autumn 2025, the Base Rate could decline to around 4%. This cautious optimism is tempered by economic factors including inflation, which remained above the Bank of England’s 2% target in recent months.

For borrowers, the implications are significant. Even modest rate changes can substantially impact monthly payments. For a £200,000 mortgage with a 25-year term, monthly payments would be £1,123 at a 4.6% rate, or £1,193 at a 5.2% rate, with even a seemingly small rate increase increasing monthly repayments by £70.

What This Means for Homeowners

The current mortgage landscape requires careful consideration. Those due to remortgage should act promptly, as the average standard variable rate is just below 8%, which is much higher than the average fixed mortgage rate. Financial experts recommend comparing deals regularly and considering professional mortgage advice to navigate the complex market.

While the trajectory suggests gradual improvement, homeowners should remain realistic. The ultra-low rates of the post-2008 financial crisis era are unlikely to return in the near term, but the market is moving towards more affordable borrowing costs as economic conditions stabilise.