FCA redress scheme: proposed motor finance compensation and implications

Introduction

The fca redress scheme has become a focal point for consumers, lenders and dealers following a Supreme Court judgment in August 2025. The Financial Conduct Authority’s consultation sets out proposals for an industry-wide approach to compensate motor finance customers who may have been harmed by inadequate disclosure of commission paid to dealers acting as credit brokers. The issue matters because the proposed approach could deliver significant consumer compensation and impose major costs and operational demands on the lending industry.

Main body

Background and trigger

On 1 August 2025 the Supreme Court handed down judgment in Johnson v FirstRand Bank Ltd, Wrench v FirstRand Bank Ltd and Hopcraft v Close Brothers Ltd. That judgment prompted the FCA to publish consultation paper CP25/27 on 7 October 2025, proposing a redress scheme for affected motor finance agreements.

Scope and criteria

The FCA proposes the scheme would cover regulated motor finance agreements taken out by consumers between 6 April 2007 and 1 November 2024 where commission was paid by the lender (or a third party) to a credit broker. The proposed coverage includes arrangements involving discretionary commissions, commissions alleged to be excessively high, and commercial ties between lender and dealer that were not adequately disclosed and so may have created ‘unfair relationships’ under the Consumer Credit Act 1974.

Remedies and calculation

If a transaction meets the scheme criteria, the consumer would be entitled to compensation and lenders would be required to calculate redress. Where an agreement involves both a very high commission (at least 50% of the total cost of credit and 22.5% of the loan amount) and a tied arrangement, the lender must apply the higher of the Commission Repayment Remedy or the APR Adjustment Remedy. The FCA also proposes a rebuttable presumption of loss or damage that lenders can challenge only with clear, contemporaneous, customer-specific evidence that the consumer could not have obtained a lower rate from other lenders the dealer dealt with at the time.

Conclusion

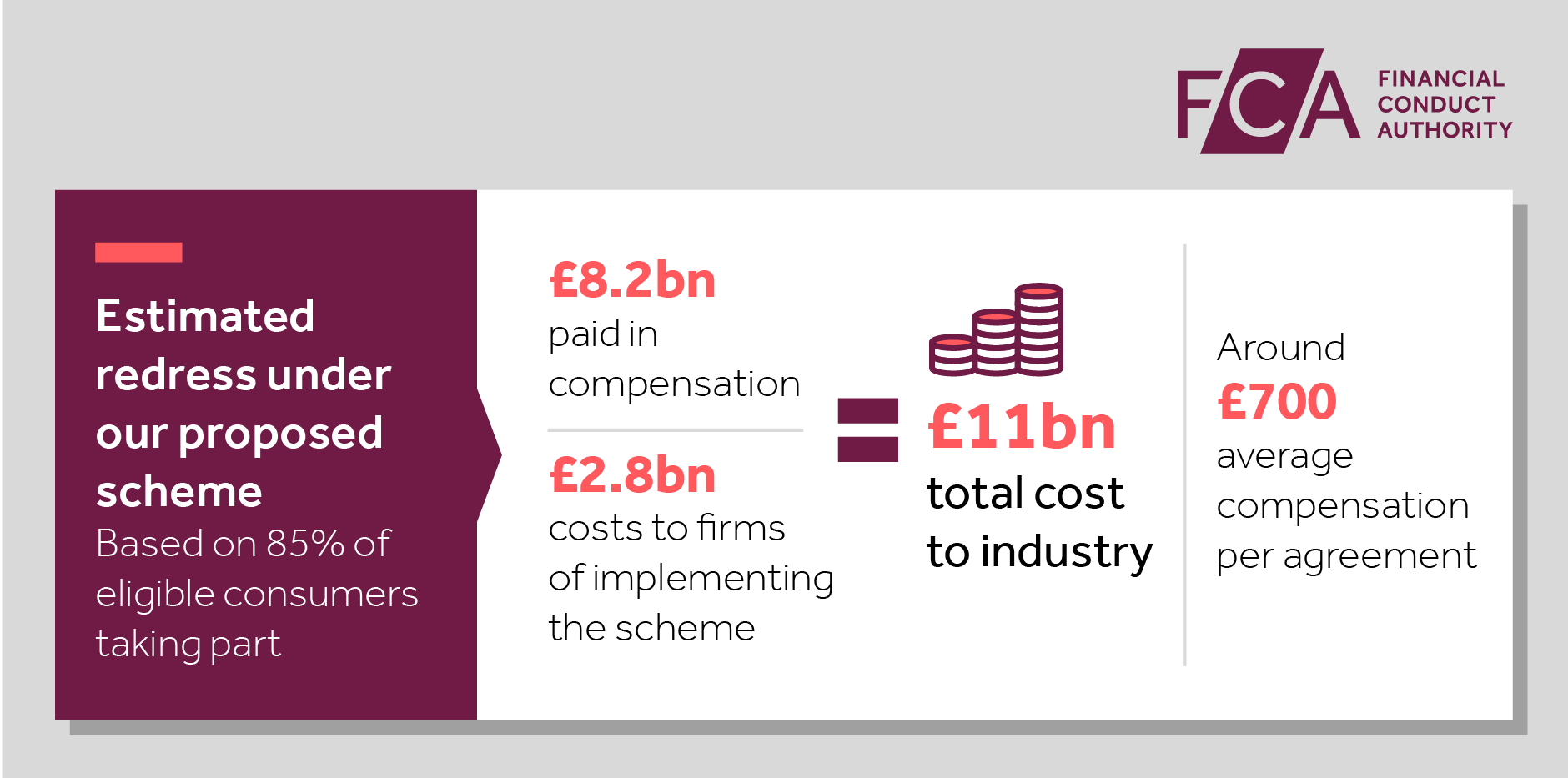

The FCA estimates the scheme could lead to around £8.2bn of compensation and a further £2.8bn of implementation costs for industry. If adopted, firms will need to review historical records, model remedies and prepare operational responses. For consumers the scheme offers a potential route to redress; for lenders and dealers it represents a substantial compliance and financial challenge. Stakeholders will now review CP25/27 responses before the FCA determines next steps and a timeline for implementation.