Fintech Innovation Drives Change Across Financial Services

Introduction: Why fintech innovation matters now

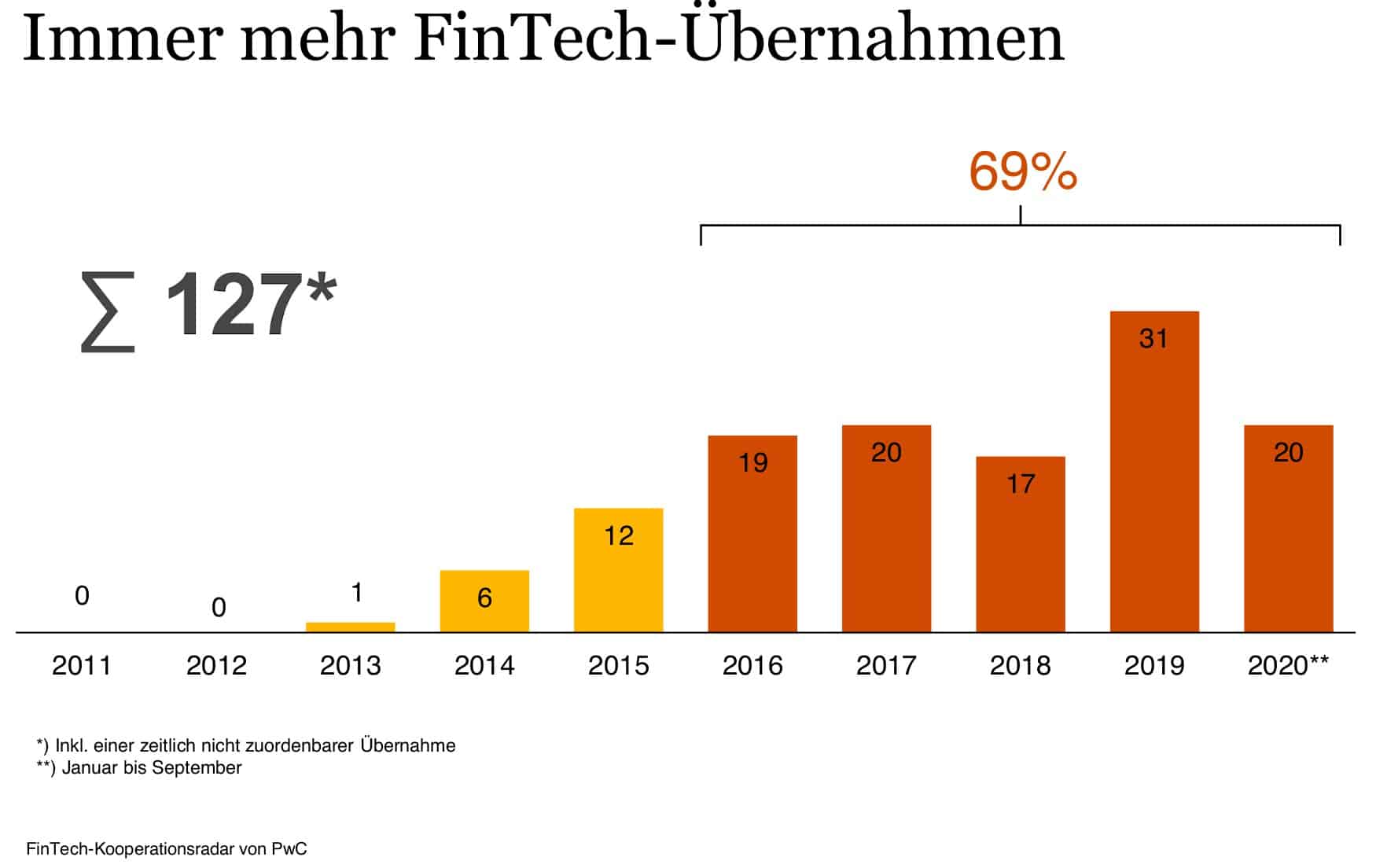

Fintech innovation has become a central topic for consumers, businesses and regulators. As digital technology reshapes how money moves, how credit is granted and how risk is managed, developments in fintech affect daily life, economic efficiency and financial stability. This story explains the significance of recent fintech trends and why readers should care about their impact on convenience, cost and security.

Main developments and facts

Digital payments and instant transfers

One prominent area of fintech innovation is digital payments. Contactless cards, mobile wallets and faster bank-to-bank transfer systems have reduced friction in retail and peer-to-peer payments. The focus for providers is on speed, interoperability and lower transaction costs, while merchants and consumers benefit from greater convenience and choice.

Credit, lending and new underwriting models

Innovation is also evident in lending. Alternative credit-scoring models use broader data sources and machine learning to assess borrower risk, allowing some previously underserved customers to access credit. Lenders increasingly combine automated decision systems with human oversight to improve efficiency while seeking to manage fairness and accuracy.

Regulation, security and consumer protection

Regulators have responded to fintech innovation by updating frameworks to balance innovation with consumer protection. Areas of regulatory focus include data privacy, anti-money laundering safeguards and operational resilience. Security remains a core concern: as services digitalise, firms invest in stronger authentication, encryption and monitoring to counter fraud and cyber threats.

Conclusion: What this means for readers

Fintech innovation promises faster services, reduced costs and broader financial inclusion, but it also brings new risks and policy challenges. For consumers, the immediate benefits are greater convenience and expanded choices; for businesses, opportunities lie in efficiency gains and new market segments. Policymakers will need to continue adapting rules to foster innovation while protecting users. Looking ahead, the trajectory suggests gradual integration of new technologies into everyday finance, with ongoing attention required on security, fairness and transparency.