Fintech Innovation: How Technology is Reshaping Financial Services

Introduction: Why fintech innovation matters

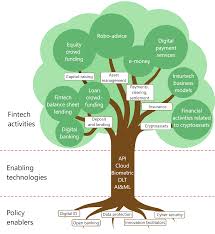

Fintech innovation has become a central force in modern finance, transforming how individuals and organisations manage money, access services and make payments. Its relevance spans consumers, small businesses and large financial institutions because technological advances can improve convenience, lower costs and broaden access to financial products. Understanding these developments helps readers assess the implications for everyday finance and commercial strategy.

Main developments and facts

Digital payments and customer experience

One of the most visible areas of fintech innovation is digital payments. Contactless cards, mobile wallets and real‑time transfers have changed expectations around speed and convenience. Businesses and consumers increasingly prefer seamless, secure payment journeys, prompting banks and payment companies to prioritise user experience and interoperability.

Open banking and data sharing

Open banking initiatives have encouraged the secure sharing of financial data between authorised providers, enabling new services such as account aggregation, personalised budgeting tools and streamlined lending assessments. This shift emphasises competition and consumer control over data while requiring robust safeguards around consent and privacy.

AI, automation and risk management

Artificial intelligence and automation are key components of fintech innovation. They are used for credit decisioning, fraud detection and customer support through chatbots and machine learning models. These tools can increase efficiency and accuracy, though they raise questions about explainability, bias and regulatory oversight.

Regulation, security and inclusion

Regulators are adapting to rapid change with measures such as sandbox environments and updated conduct rules. Cybersecurity remains a critical concern as the attack surface expands with digital services. At the same time, fintech innovation presents opportunities to improve financial inclusion by lowering barriers for underserved populations, provided solutions are designed with accessibility in mind.

Conclusion: Implications and outlook

Fintech innovation is not a single event but a continuing process that blends technology, regulation and market demand. For consumers, it promises greater convenience and choice; for businesses, new competitive pressures and partnership opportunities; and for regulators, the task of balancing innovation with protection. Observing these trends will help readers anticipate how financial services are likely to evolve and what changes may affect everyday financial decisions.