Fintech innovation: models, patents and bank collaboration

Introduction: Why fintech innovation matters

Fintech innovation is central to the ongoing transformation of financial services. New business models, intellectual property strategies and cross‑sector partnerships are changing how consumers and firms access payments, credit and wealth services. Understanding these forces matters for regulators, incumbents and customers because they determine who will lead the next phase of disruption and what services will become widely available.

Main developments driving change

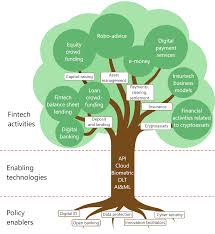

Ten disruptive business models

According to the Board of Innovation (BOI), there are ten innovative FinTech business models that are leading the path of disruption. These models illustrate diverse approaches to serving customers, from platform‑based offerings to embedded finance and specialised niche services. BOI’s framework highlights how different models challenge traditional banking assumptions and create new routes to revenue and customer engagement.

Patents, collaboration and competitive dynamics

PatSeer emphasises that fintech isn’t just about apps and algorithms; it is a complex ecosystem driven by innovation, collaboration and fierce competition. Patents play a critical role: they act as the DNA of the ecosystem by protecting inventions and shaping how firms invest in technology. At the same time, collaboration—between fintech startups, technology firms and established financial institutions—can accelerate adoption while influencing how intellectual property is shared or licensed.

Why major banks struggle and the role of partnerships

Reports on bank–fintech collaboration point to clear reasons why major banks often struggle to innovate at pace. Cultural barriers, legacy technology and organisational structure can slow change. The analysis underlines the importance of developing a spirit of innovation, engaging in technology development and actively partnering with fintech firms. Effective partnerships can combine banks’ regulatory experience and customer bases with fintech agility and specialised technologies.

Conclusion: What this means for readers

Fintech innovation is being propelled by distinct business models, strategic use of patents and collaborative approaches. For customers, this promises more tailored and accessible services; for banks, it signals the need to adapt through partnerships and internal change. Going forward, expect continued experimentation across the ten model archetypes, increased emphasis on intellectual property strategy, and deeper bank–fintech collaboration as the primary route for incumbents to remain competitive.