How fintech innovation is reshaping financial services

Introduction: Why fintech innovation matters

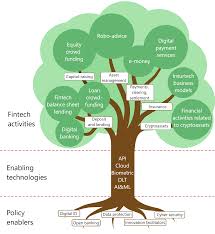

Fintech innovation is central to how people and businesses access, manage and move money. Its relevance spans consumers, small enterprises and large institutions because technological advances can lower costs, broaden access and change regulatory expectations. Understanding current fintech trends helps readers assess risks and opportunities in payments, lending, data sharing and customer experience.

Main developments in fintech innovation

Digital payments and wallets

Contactless payments, mobile wallets and real‑time settlement are now mainstream in many markets. These solutions reduce friction at the point of sale and encourage cashless behaviour. For businesses, the shift brings efficiency gains but also a need to manage digital security and interoperability between providers.

Artificial intelligence and automation

AI and machine learning are being deployed across credit scoring, fraud detection and customer service. Automation improves decision speed and consistency, while advanced analytics enable more personalised offers. Organisations must balance accuracy with fairness and transparency to maintain consumer trust and meet regulatory expectations.

Open banking and data portability

Open banking standards encourage secure data sharing between authorised providers, enabling new services such as account aggregation and tailored lending. This promotes competition and innovation but requires robust consent frameworks and strong data protection measures.

Embedded finance and platformisation

Non‑bank platforms are increasingly embedding financial services—payments, insurance, lending—directly into consumer experiences. This creates convenience and new revenue streams, while raising questions about oversight, consumer protection and the distribution of risk across ecosystems.

Conclusion: What readers should take away

Fintech innovation continues to accelerate an ongoing transformation of the financial sector. For consumers, the benefits include greater convenience, faster services and potentially lower costs; for businesses, new distribution models and efficiency gains. However, these advances bring heightened focus on regulation, security and fairness. Looking ahead, expect further convergence of technology and finance, with regulators and industry participants adapting to ensure innovation remains trustworthy and inclusive. Readers should watch developments in data governance, AI practice and cross‑border payment standards as indicators of how the next phase of fintech innovation will unfold.