Lloyds Banking Group’s role in UK banking and recent developments

Introduction: Why Lloyds Banking Group matters

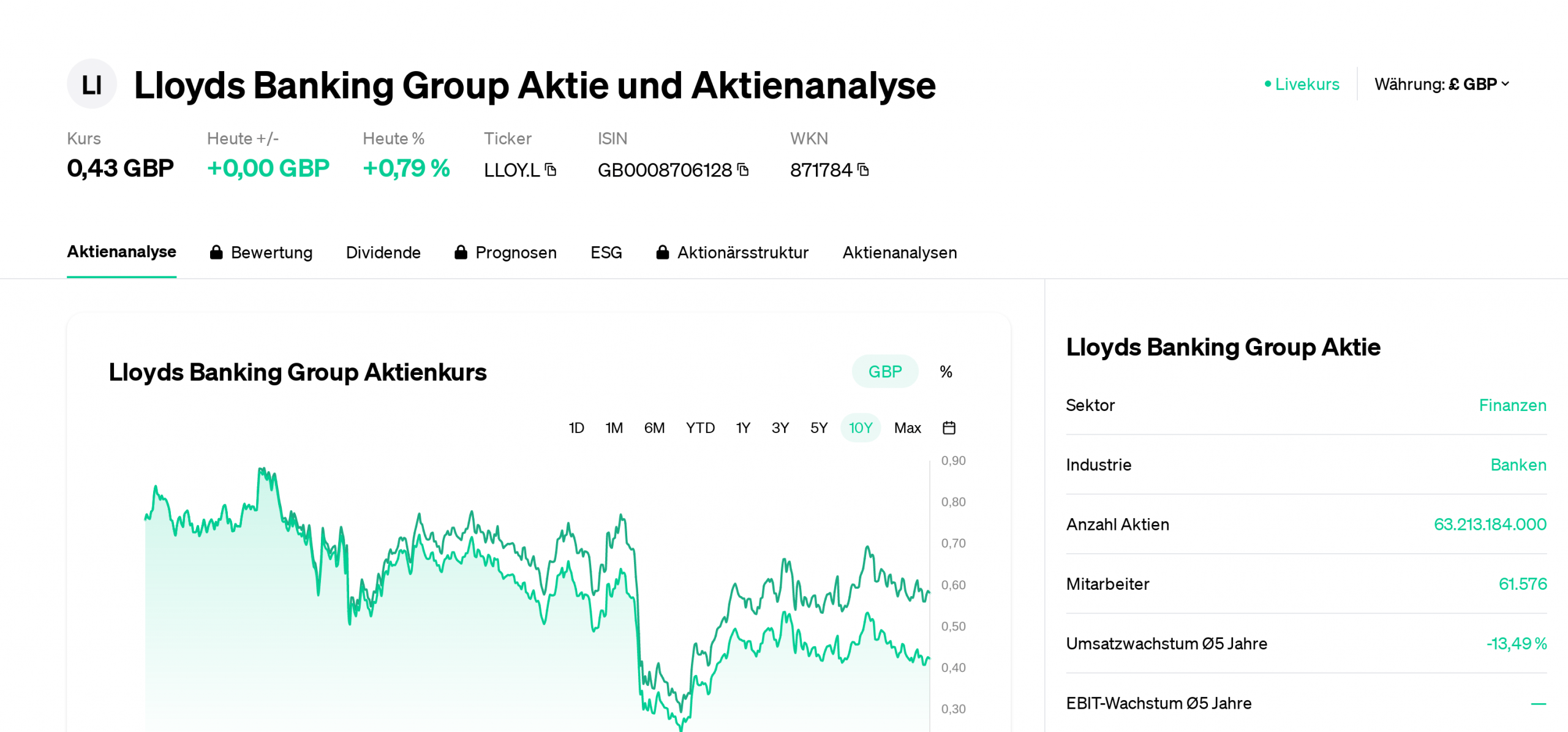

Lloyds Banking Group is a central player in the United Kingdom’s financial system. Its size, customer base and history of government intervention make it relevant to consumers, businesses and policymakers. Understanding the group’s formation, state ownership legacy and current positioning helps explain broader trends in UK banking and public finance.

Main developments and facts

2008–2009: Rescue and formation

In October 2008, Prime Minister Gordon Brown announced a government plan for the Treasury to invest £37 billion into major UK banks including Royal Bank of Scotland Group, Lloyds TSB and HBOS to avert a collapse of the financial sector. Following those recapitalisations and Lloyds TSB’s acquisition of HBOS, Lloyds Banking Group was established in 2009 as a consolidated British financial institution.

Government ownership and subsequent sales

After the rescue and the acquisition, the UK government held a 43.4% stake in Lloyds Banking Group. That large holding reflected the scale of public support provided during the crisis. By 2013 there were moves to reduce this stake: in February 2013 reports noted that Lloyds was considering a stock market flotation of its TSB business as an alternative, and in September 2013 the government was reported to be planning to sell up to a quarter of its shares in the group.

Current position and stated purpose

Today Lloyds Banking Group describes itself as the largest UK retail and commercial financial services provider, serving 26 million customers and maintaining a leading digital presence. The group’s stated purpose, as presented on corporate channels, is ‘Helping Britain Prosper’, emphasising commitments to sustainability, inclusion and shaping finance as a force for people and businesses.

Conclusion: Significance and outlook

Lloyds Banking Group’s history from crisis-era rescue to large-scale retail provider underlines its systemic importance. The reduction of state ownership in the 2010s signalled a return towards private ownership, while the group’s scale and digital focus point to its continued influence on UK banking. For customers and businesses, developments within Lloyds will remain significant for access to financial services and for broader market confidence; for policymakers, the group’s trajectory offers lessons about crisis intervention and subsequent privatisation choices.