Mortgage rates today: what borrowers need to know

Introduction — Why mortgage rates today matter

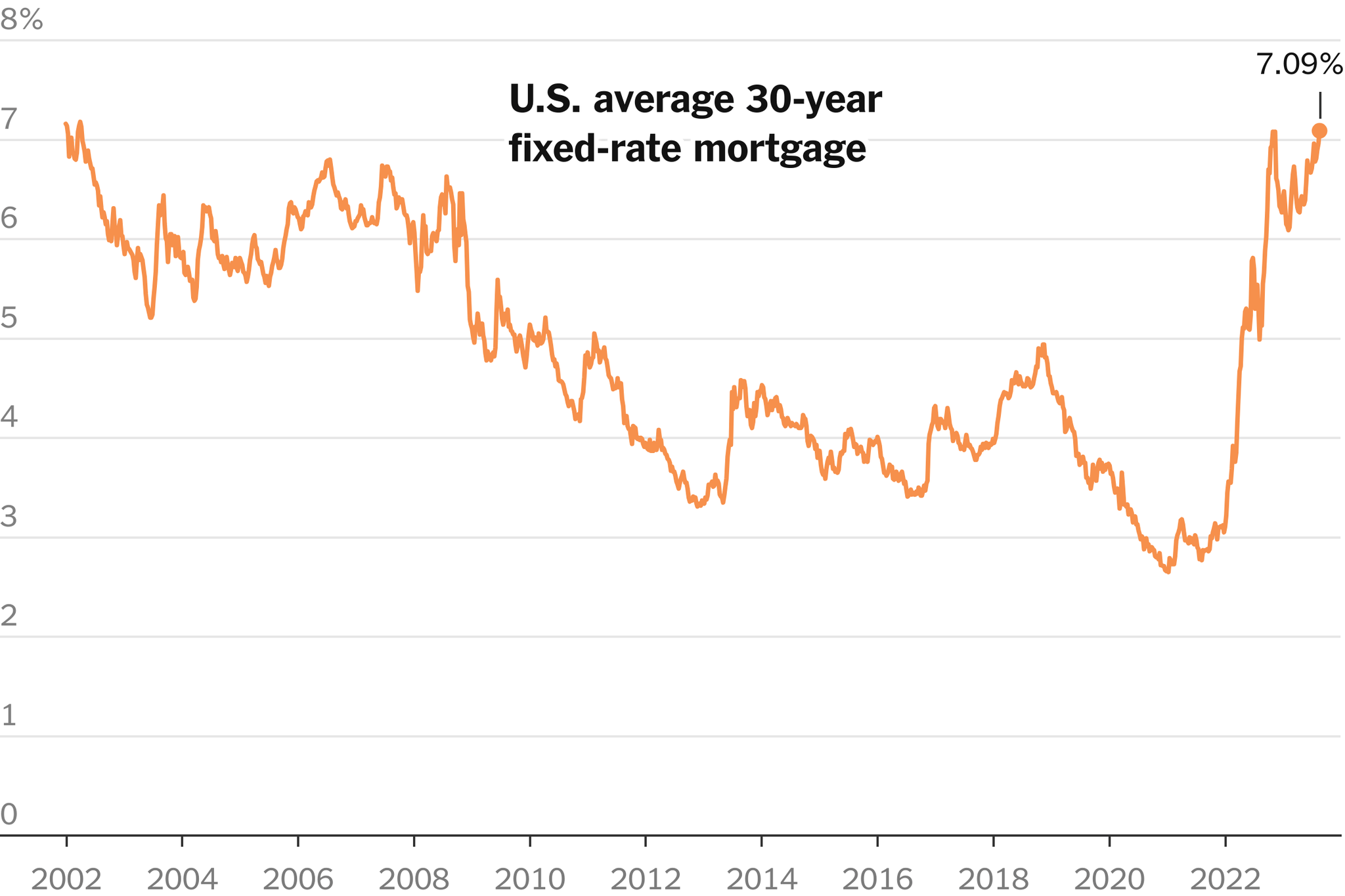

Mortgage rates today are a central concern for homebuyers, homeowners considering remortgaging and the wider housing market. Small shifts in rates can materially affect monthly payments, affordability and long-term housing decisions. Given the sensitivity of household budgets and financial planning to borrowing costs, clear, timely information on mortgage rate movements remains important for consumers and policymakers alike.

Main developments and drivers

Underlying economic influences

Movements in mortgage rates typically reflect expectations about central bank policy, inflation trends and broader economic growth. When inflation is persistent, central banks may raise policy rates to cool price pressures, which tends to push mortgage rates higher. Conversely, signs of slowing inflation or weaker growth can ease monetary policy expectations and put downward pressure on borrowing costs.

Market and lender dynamics

Mortgage rates today also respond to funding costs in wholesale markets and to competition among lenders. Banks and mortgage providers set retail mortgage offers by adding margins to their own borrowing costs, so shifts in market yields, investor demand for mortgage-backed securities and lenders’ risk appetites all feed through to the rates available to borrowers.

Product types and borrower impact

Fixed-rate and variable-rate products behave differently. Fixed rates lock in a rate for a set period and shield borrowers from short-term volatility, while variable and tracker rates move more closely with short-term interest rate expectations. For prospective buyers, the choice between these products depends on budget certainty, outlook for rates and individual risk tolerance.

Conclusion — What this means for readers

For readers, the practical takeaway is to monitor mortgage rates today in conjunction with economic indicators and lender offerings. Those seeking to buy or remortgage should compare products, consider the benefits of rate protection versus flexibility, and, where appropriate, consult a mortgage adviser. While short-term rate movements are difficult to predict precisely, understanding the main drivers can help households make more informed borrowing decisions and plan for possible changes in monthly costs.