Mortgage Rates Today: What Borrowers Need to Know

Introduction — Why mortgage rates today matter

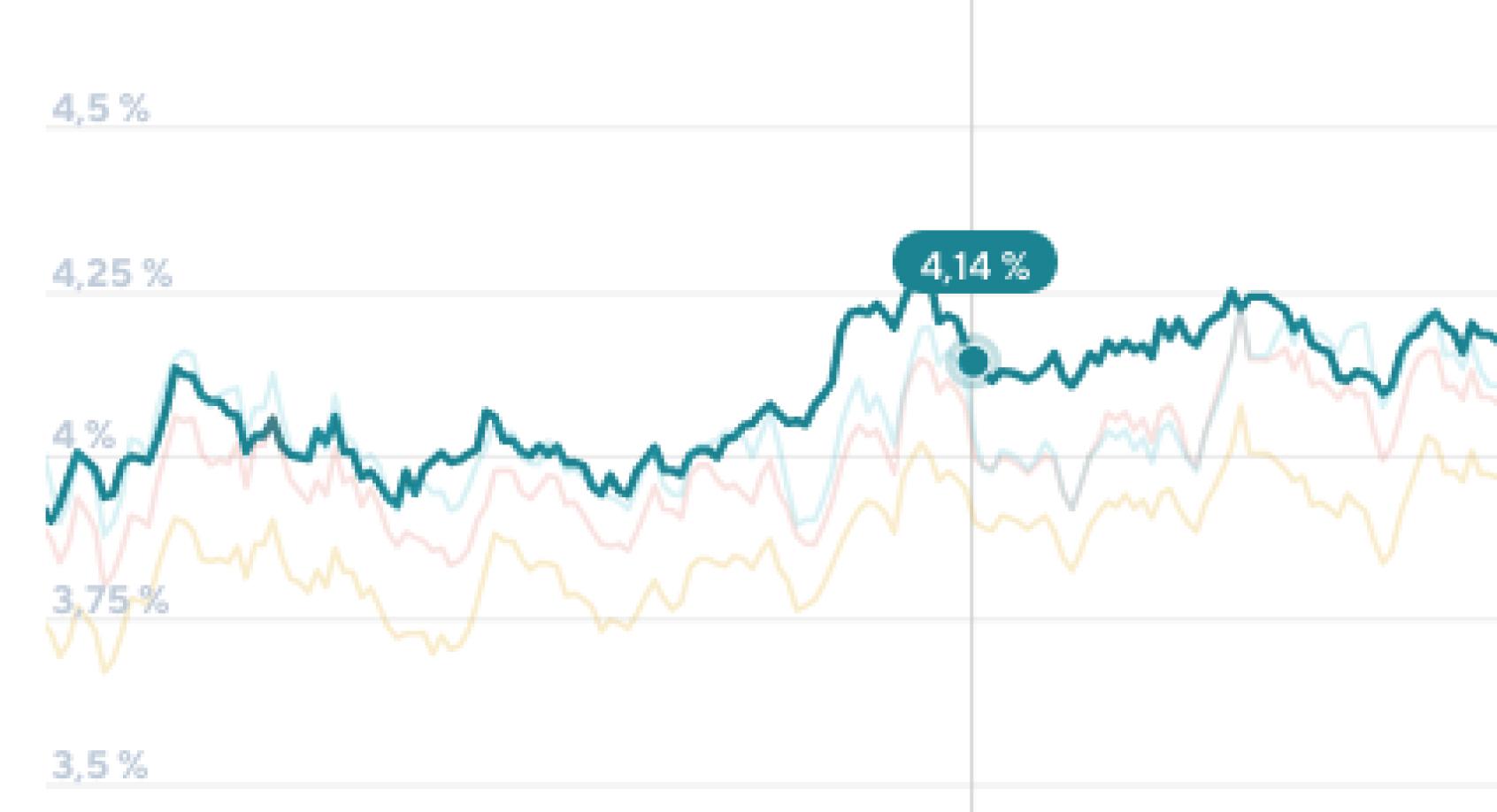

Mortgage rates today are a central concern for anyone buying, remortgaging or budgeting for housing costs. Movements in mortgage rates affect monthly payments, the affordability of new purchases and household budgets across the UK. For homeowners and prospective buyers alike, understanding the forces behind rate changes helps inform timing and product choice.

Main developments and driving factors

Monetary policy and central bank influence

The Bank of England’s policy decisions are a primary influence on mortgage pricing. When the central bank adjusts its base rate in response to inflation or economic conditions, lenders typically reprice variable-rate products and influence the wider yield curve that underpins fixed-rate deals. Consequently, borrowers watching mortgage rates today should pay attention to official communications and inflation data.

Bond markets and lender margins

Longer-term fixed rates are closely tied to government bond yields. Movements in gilt yields, driven by expectations for growth and inflation, feed into the cost at which lenders secure wholesale funding. Lenders then add margins reflecting credit risk and competition. These components together determine the mortgage rates consumers see advertised.

Housing market activity and demand

Demand for loans and the broader housing market climate also shape mortgage pricing. Strong demand for mortgages can lead to tighter lending criteria or slightly higher rates, while subdued activity may prompt competitive pricing. Borrower credit profiles—deposit size, income stability and credit history—remain key determinants of the specific rate an individual can secure.

Conclusion — What readers should take away

Mortgage rates today fluctuate for multiple reasons: central bank policy, bond markets, lender strategy and housing demand. For borrowers, the practical steps are consistent—shop across lenders, check fixed versus variable options, consider the length of the term and assess the costs of switching or early repayment. Keeping an eye on official economic indicators and seeking personalised advice can help households make decisions appropriate to their circumstances. In a changing market, clarity about one’s budget and priorities remains the most reliable guide.