Understanding council tax: charges, exemptions and surcharges

Introduction

Council tax is a central element of local public finance in the UK. It is a domestic property tax collected by local councils that helps fund essential local services such as waste collection, schools, social care and community facilities. Understanding how council tax works, who is liable to pay, and recent changes to powers over empty properties and second homes is important for homeowners, landlords and tenants.

Main details

How council tax works

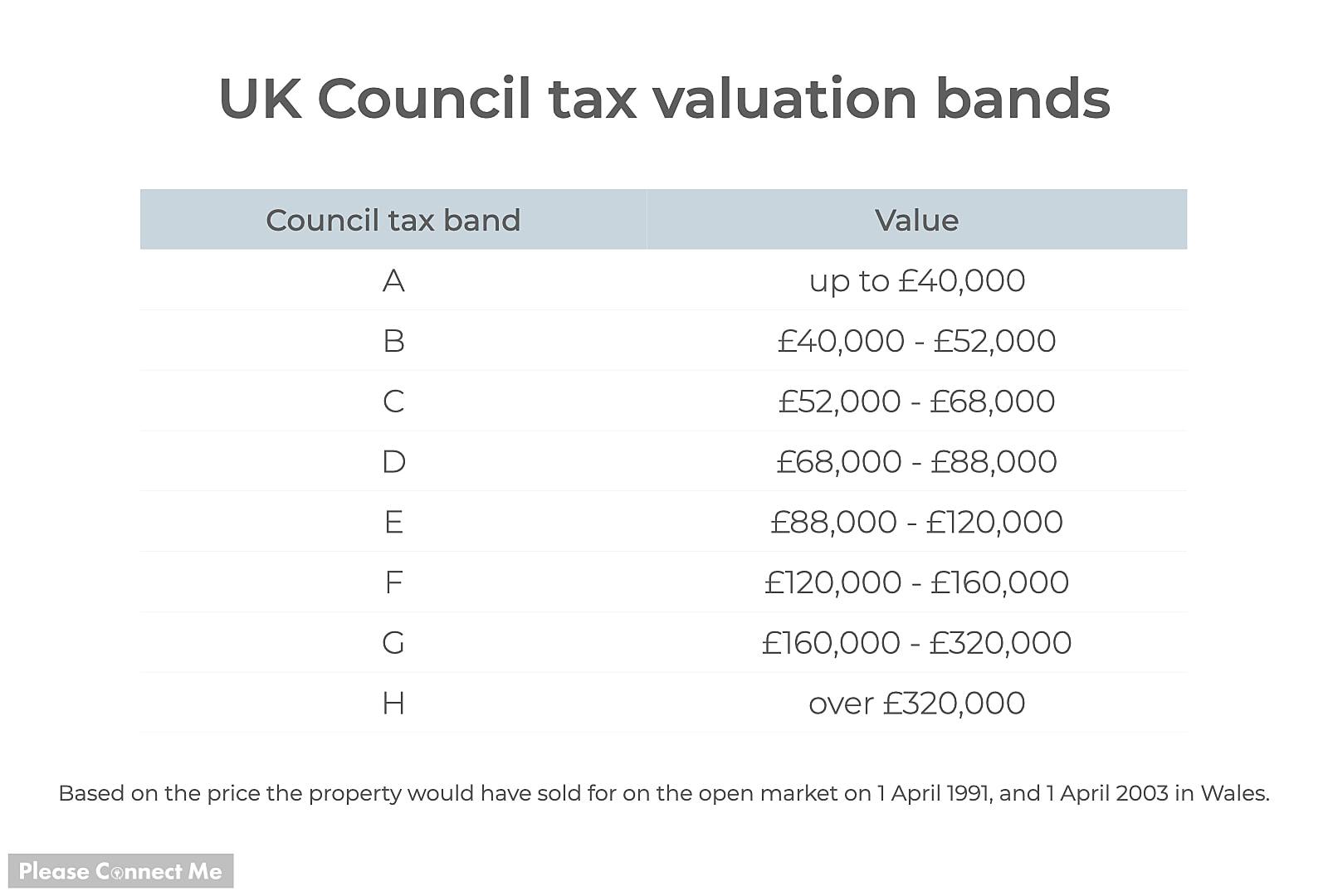

Council tax is charged annually and set by each local council. The amount payable depends on factors determined locally, including the property’s valuation band and the council’s chosen rates. Payments contribute directly to the funding of local services and budgets under the control of the billing authority.

Who pays and exemptions

Liability for council tax typically rests with the resident or owner of a domestic property. Some properties are exempt from council tax — for example certain unoccupied or specially used dwellings — and discounts or reductions can apply in specific circumstances. People unsure about liability or entitlement to relief are advised to check guidance from Citizens Advice or the relevant local authority.

Surcharges, empty homes and second homes

Beginning in the 2010s, the UK Government and devolved administrations in Scotland and Wales introduced powers for billing authorities to levy surcharges on particular property types. These include long-term empty dwellings and dwellings occupied periodically, commonly described as second homes or holiday homes. In Wales, the Housing (Wales) Act 2014 provided for billing authorities to levy a council tax surcharge of up to 100% on properties empty for more than one year or used as second homes. Further measures affecting empty-dwelling surcharges are reflected in legislation such as the Rating (Property in Common Occupation) and Council Tax (Empty Dwellings) Act 2018.

Conclusion

Council tax remains a locally determined, central source of revenue for local authorities. Recent legislative changes have broadened councils’ powers to discourage long-term empty properties and to raise additional revenue from second homes. For property owners and occupiers, staying informed about local council policies, possible exemptions and surcharges is essential to understanding liability and potential savings.